- Discover What is Algo Trading: Pros and Cons in this comprehensive guide. Learn how automated trading systems function, explore top strategies, and weigh the benefits against technical risks.

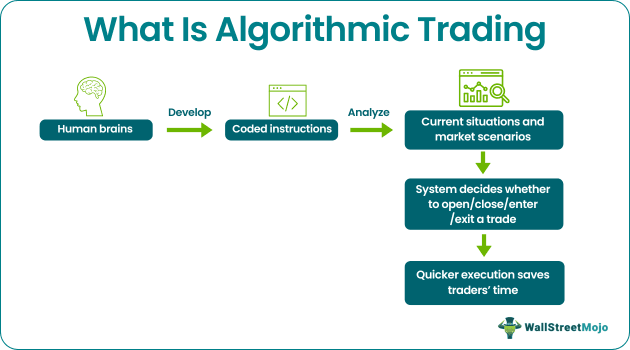

Algorithmic trading is the process of executing financial transactions through computer programs that follow a predefined, automated set of instructions. Driven by advanced mathematics and structural software code, these digital systems monitor live market variations and execute orders without manual human intervention.

By deploying logic-based criteria such as price levels, specific timing intervals, trading volume, or mathematical models, algorithms process massive data streams in milliseconds. While historically restricted to institutional hedge funds, algorithmic architectures now serve retail market participants looking to eliminate emotional bias and maximize structural execution speed across global asset classes.

How Does Algorithmic Trading Work?

The mechanics of algorithmic execution rely on converting a logical trading thesis into binary computer code. Rather than interpreting a live chart subjectively, a computer program systematically evaluates real-time market data against rigid parameter baselines.

To understand how algorithmic trading works from development to live deployment, the process follows five structural phases:

- Formulate Strategy: Establishing a repeatable market edge based on technical, fundamental, or statistical quantitative criteria.

- Backtest Architecture: Running the specific coded rules against historical market data to verify the hypothetical profitability and risk parameters of the system.

- Deploy Integration: Connecting the algorithmic code to a live brokerage account via a secure Application Programming Interface (API).

- Automated Execution: The software continuously scans live price feeds, immediately sending market orders to the exchange the moment all programmed parameters match.

- System Supervision: Monitoring the hardware infrastructure, data feeds, and execution latency to prevent mechanical or connectivity disruptions.

Core Components of an Algorithmic Trading System

An enterprise-grade automated trading setup requires a synthesis of structural hardware, programmatic logic, and data verification filters to function reliably in live market conditions.

- Programmatic Code Rules: The software logic built using technical if-else statements or complex mathematical formulas to define market entries and exits.

- Network Connectivity Infrastructure: Low-latency servers and virtual private networks that keep the execution platform synchronized with live exchange data.

- Technical Data Feeds: Continuous, high-speed streams of price, liquidity, and order-book metrics that feed into the processing engine.

- Historical Backtesting Engine: A secure sandbox environment containing clean historical data used to expose software bugs and evaluate strategy drawdowns.

Popular Strategies in Algorithmic Trading

Automated models use distinct mathematical and statistical methodologies to extract capital from global exchanges. Below are the most prevalent algorithmic trading strategies deployed in modern financial markets.

Trend Detection Strategies

Trend detection is the most common algorithmic approach, focusing on tracking and riding sustained market momentum.

- The Logic: Programs scan thousands of assets simultaneously to identify prevailing directional trends using indicators like moving average crossovers, channel breakouts, or price-momentum metrics.

- Execution: The algorithm opens a long position when short-term momentum accelerates upward and exits automatically when price structural patterns show signs of a technical breakdown.

Mean Reversion Strategies

Mean reversion operates on the mathematical premise that asset prices will ultimately return to their historical average or mean over time.

- The Logic: The program tracks the statistical standard deviation of an asset’s price away from a baseline moving average.

- Execution: When an asset is deemed statistically overextended (either severely overbought or oversold), the algorithm executes a counter-trend position, betting that the price will snap back toward its average level.

Statistical Arbitrage

Arbitrage strategies exploit temporary structural price discrepancies for the exact same asset across different geographical exchanges or related financial instruments.

- The Logic: The system monitors dual-listed instruments, searching for brief valuation mismatches that occur during volatile trading periods.

- Execution: The algorithm instantly purchases the asset on the lower-priced exchange and simultaneously sells it on the higher-priced exchange, locking in a risk-free profit before the discrepancy corrects.

Index Fund Rebalancing

Index funds must periodically adjust their holdings to accurately reflect the changing market capitalizations of their underlying assets.

- The Logic: Algorithms anticipate the exact timing and volume requirements of these institutional portfolio rebalancings.

- Execution: Automated systems buy or sell the affected equities just ahead of the fund’s scheduled rebalancing window, capitalizing on the guaranteed liquidity and predictable price movements.

Pros of Algorithmic Trading

Automating financial execution offers distinct technical advantages over conventional, manual trading methodologies.

- Superior Execution Speed: Algorithms analyze market metrics and transmit orders in milliseconds, achieving optimal fill prices and minimizing slippage.

- Elimination of Human Error: Automated systems remove psychological vulnerabilities such as fear, greed, or hesitation, sticking purely to objective rule-based logic.

- Simultaneous Automated Checks: Computers can cross-reference multiple technical indicators, volume spikes, and macro correlations across dozens of charts at the same time.

- Reduced Transaction Costs: By automating large institutional block trades, algorithms cut routing inefficiencies and optimize transaction expense structures.

- Backtesting Capability: Traders can comprehensively audit a strategy’s statistical validity on decades of historical data before risking live capital.

Cons of Algorithmic Trading

Despite its technical efficiency, automation introduces unique systemic risks and operational challenges that market participants must manage.

- Technology Dependency: Automated systems are highly vulnerable to software bugs, API disconnects, connectivity failures, and server power outages that can trigger unintended market orders.

- Risk of Over-Optimization: Curve-fitting a strategy too closely to historical data can create a program that looks flawless in backtests but fails catastrophically in live, evolving markets.

- Systemic Market Impact: Large-scale institutional algorithms executing simultaneously can trigger extreme price flash crashes or cause sudden liquidity vacuums.

- Regulatory Challenges: Global financial authorities enforce strict compliance rules and implement mandatory circuit breakers to limit the functionality of erratic algo-trades.

- High Capital Costs: Developing and maintaining proprietary software, data feeds, and low-latency virtual private servers demands significant financial resources.

- Lack of Human Judgment: Purely computerized models rely on historical data patterns and cannot apply intuitive “gut check” judgment during unprecedented macroeconomic black swan events.

Yes, algorithmic trading is entirely legal across most major global financial markets. Regulatory bodies establish strict oversight guidelines for automated platforms to ensure market integrity, often utilizing algorithmic circuit breakers to halt trading during sudden, unexpected spikes in market volatility.

A flash crash is a rapid, deep decline in asset prices within an incredibly short timeframe, often caused by high-frequency trading algorithms pulling liquidity or entering a feedback loop of simultaneous automated sell orders.

No, algorithmic trading does not guarantee profitability. An automated trading program simply executes the underlying human logic at high speeds; if the trading strategy’s logic is fundamentally flawed or poorly managed, the algorithm will simply accelerate and multiply capital losses.