Over the past month, IAG’s stock price has declined quite a bit, from 395.80p on August 23, 2025, to 379.10p as of this writing. This is a loss of roughly 4%. The company’s long-term growth has mostly been positive, but recent downward pressure seems to be caused by a mix of macroeconomic factors and problems specific to the business.

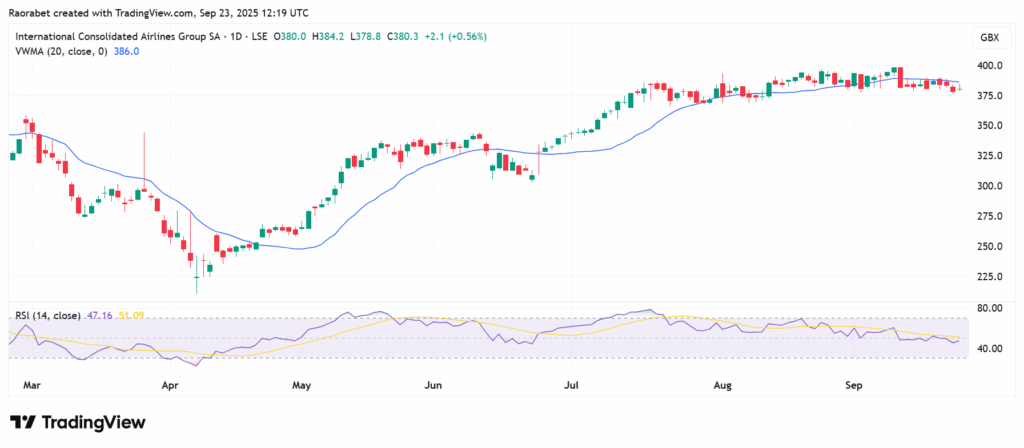

IAG stock price is on a weak momentum below the Volume Weighted Moving Average (VWMA) and its RSI is below 50 on the daily chart. Source: TradingView

Why is IAG Stock Price Declining?

IAG stock price rose to record highs barely a month ago, but several interconnected elements are exerting pressure on the declining trend. When IAG released its Q2 earnings in August, investors were unhappy that it didn’t improve its full-year guidance, even though it reported solid results with operating profit up 35% to €1.68 billion. This dampened excitement as the company said it was being cautious about the H2 performance because travel demand could drop down.

Investors have been scared off by growing US prices, a dimming employment picture, and concerns of decreased demand for transatlantic travel, all of which have put a strain on the economy, especially in the crucial North American market.

High operational costs are another big problem for IAG (LSE: IAG) that won’t go away. The airline conglomerate has made a lot of progress in increasing its profit margins through substantial transformation program after the pandemic, but the airline industry is still subject to outside shocks. Geopolitical events, especially those with an impact on global oil prices, can significantly impact an airline’s profits because fuel is a major cost.

In addition, uncertainty is heightened by global threats, such as the possibility of new tariffs and persisting issues with the supply chain. There is also a tightening competition in the airline industry, which makes it hard to set prices. Non-fuel unit costs are likely to go up by 3% this year, although that is less than initial forecasts. Investors are also concerned about rising inflation, which could raise operation costs significantly.

What Will It Take for IAG Stock to Recover?

For IAG’s stock price to go up again, a number of things will have to merge. First and foremost, there needs to be a more stable outlook for the global economy. A drop in inflation, especially in important markets like the UK and Europe, would reduce the strain on consumers’ disposable income and, by implication, on travel demand. Also, IAG stock price could benefit from any hint that the US Federal Reserve would lower interest rates in the fourth quarter. That could potentially boost confidence by making it cheaper for the company to borrow money in the future and generally promoting investment in cyclical sectors.

Also, if oil prices stabilize or go down, it would lower costs and raise margins. This would build on IAG’s strong long-haul pricing strength and capacity discipline. Ultimately, a recovery depends on both the economy becoming better and IAG’s ability to keep meeting its operational and financial targets.

Also, good news regarding future earnings, like improving projections or cutting costs even more, could improve investors sentiment about the company. The continuation of shareholder payouts, such as the €1 billion buyback in 2025 and the return to dividends (with an expected yield of approximately 2%), would indicate a strong financial position.

The stock has declined due to a broader market downturn, concerns over a slowing economy, high operational costs from fuel prices, and intense competition from other airlines.

For IAG stock price to recover, it will need favourable upturn in operating conditions, primarily including lower oil prices, stronger US economy, positive earnings updates, and continuation of share buybacks.

IAG stock currently carries moderate risk despite its recent decline. Even though large debt is its biggest limiter, the stock is still undervalued relative to its peers. These factors when looked at holistically call for a cautious purchase.

This article was originally published on InvestingCube.com. Republishing without permission is prohibited.