- Barclays stock rose by more than 50% in 2025 but has struggled to stay on the upside in 2026, gaining less than 2% YTD

- The bank reported strong earnings in Q4 2025 and has raised its 2026 income forecast to £31 billion

- Barclays competitors like Lloyds and Natwest could potentially outperform it at the stock market in 2026 as market dynamics change

This week, the UK banking sector felt pressure due to shifting interest rate expectations. Barclays released its full-year 2025 earnings, and while the stock is up just over 1% year-to-date and trading around 306p as of February 12, a big change from its 57% jump in 2025, the earnings numbers tell a more interesting story.

Strong Earnings, But BARC Stock Stays Flat

Barclays announced a £9.1 billion pre-tax profit for 2025, a 12% rise year-over-year, which met analyst expectations. The bank also upped its 2026 total income forecast to £31 billion from £30 billion. The earnings report showed investment banking income rose 11% to £13 billion, with Global Markets revenue up 15%.

A disappointment, though, was pausing buybacks to fix the balance sheet, which revealed debt at £26 billion. Despite earnings suggesting power, the 1.8% dividend yield is lower than NatWest’s 3.8%, which could make it less attractive to investors if rates drop further.

Why Barclays Still Offers Better Prospects than Trail Lloyds and NatWest?

Compared to Lloyds and NatWest, Barclays’ outlook appears mixed. Lloyds, up 4.90% YTD with earnings coming February 18, expects a 20% RoTE by 2028. NatWest, with earnings due February 13, has a 3.8% yield and a 12.5 P/E ratio. NatWest has been a favorite since 2025, but its recent £2.7 billion deal for Evelyn Partners and high valuation hint that most of the gains are already factored in.

While many expect all banks to gain from the rate environment, Barclays might not do as well if markets favor the domestic focus of Lloyds and NatWest. But Barclays has a different plan. While Lloyds and NatWest have done well with UK mortgages, Barclays is focused on its diversified strategy: UK retail, corporate banking, and a big investment bank. The investment bank saw intermediation revenues climb 13%, which proves Barclays benefits when markets are unstable.

Barclays Stock Price Forecast

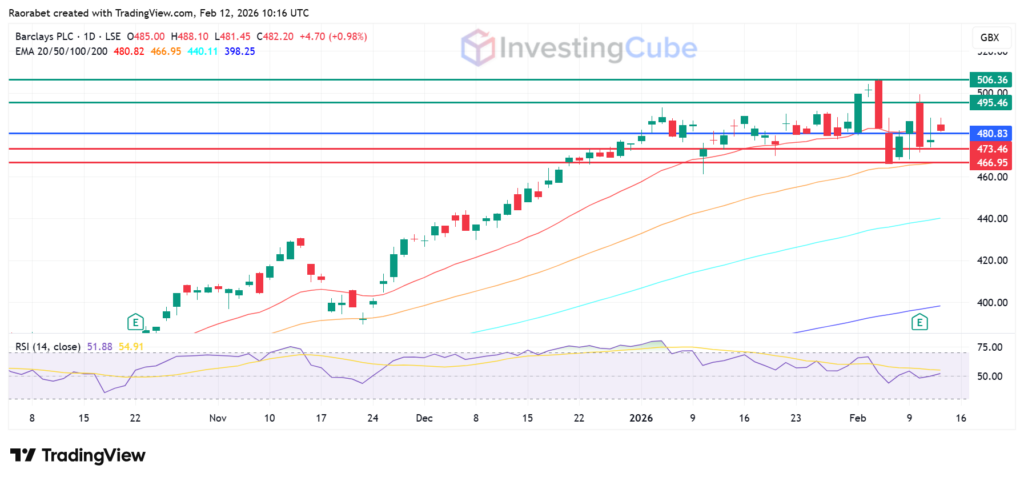

Barclays share price RSI is around 51, showing a neutral to slightly negative outlook. The upside will likely continue if the stock stays above the 20-day EMA at 480.83p. Primary resistance will likely be at 495.46, beyond which it could target 506.36. If it goes below the pivot, immediate support is at 473.46p, with a lower level at the 50-day EMA of 466.95p.

Barclays share price on the daily chart with key support and resistance on February 12, 2026. Created on TradingView

Profit-taking after 57% 2025 rise, earnings showing 12% profit growth but buyback halt for debt repair; challenges consensus strength, noting margin erosion risks from rates.

Investors are considering potential rate cuts by the Bank of England, which could lower net interest margins. Also, Barclays’ investment bank needs more capital, which some see as a disadvantage compared to the simpler models of Lloyds.

By increasing its 2026 income target to £31 billion, Barclays is confident in its structural hedge and US credit card growth. This means the bank thinks it can still grow revenue even if the Bank of England cuts interest rates.