- Barclays stock was among the biggest gainers of 2025, gaining 78%

- The Bank of England is likely to be more dovish in 2026,which could limit its Net Interest Margin (NIM)

- Barclays faces domestic competition from the likes of NatWest and Lloyds which could offer investors better returns

Barclays stock, which did very well on the London Stock Exchange in 2025 with a 78% jump driven by a 23% earnings increase to £8.1 billion, hasn’t started 2026 so well. So far this year, shares have gone down more than 2%, trading at about 482p as of now, and they dropped 4% in the past month. Does this mean a bigger fall is coming, or is it just a break after big gains?

Why Barclays Stock is Off to a Weak Start

The drop seems related to people taking profits and adjusted earnings predictions. After a great 2025, analysts have lowered the 2026 and 2027 earnings estimates by 4%, because they’re worried about non-interest income and share count going up from fewer buybacks, according to Barclays’ own report.

Another thing is the change in what people expect from interest rates. In February, the Bank of England voted 5-4 to keep rates at 3.75%, but the tone suggested that more cuts are coming in 2026. For a bank like Barclays, which makes a lot of money from Net Interest Margin (NIM), the idea of lower rates isn’t good for earnings growth.

Barclays vs. Lloyds and NatWest

Will Barclays do worse than other banks this year? That’s what the market seems to think. Compared to Lloyds Bank and NatWest, Barclays might not do as well if it doesn’t perform well. Many analysts are moving back to Lloyds Banking Group, because it makes more capital and has a higher dividend yield.

Barclays’ plan to return £10 billion through 2026 with buybacks might not be enough if defaults go up. Because Barclays is exposed to competition, it might not do as well as Lloyds if Lloyds does better with domestic stability.

On the other hand, the environment might mean Barclays is in a better spot than Lloyds for a 2026 recovery because it has a diversified Investment Bank. Lloyds is basically tied to the UK mortgage market, but Barclays benefits from the recovering economy. If investment banking fees in the US and Europe go up as Morgan Stanley expects, Barclays could easily outperform its rivals that focus more on the UK in the second half of the year.

Investors should pay attention to the February 10 strategic update. If management increases the Return on Tangible Equity (RoTE) target to around 15%, that will be a good sign.

Barclays Stock Prediction

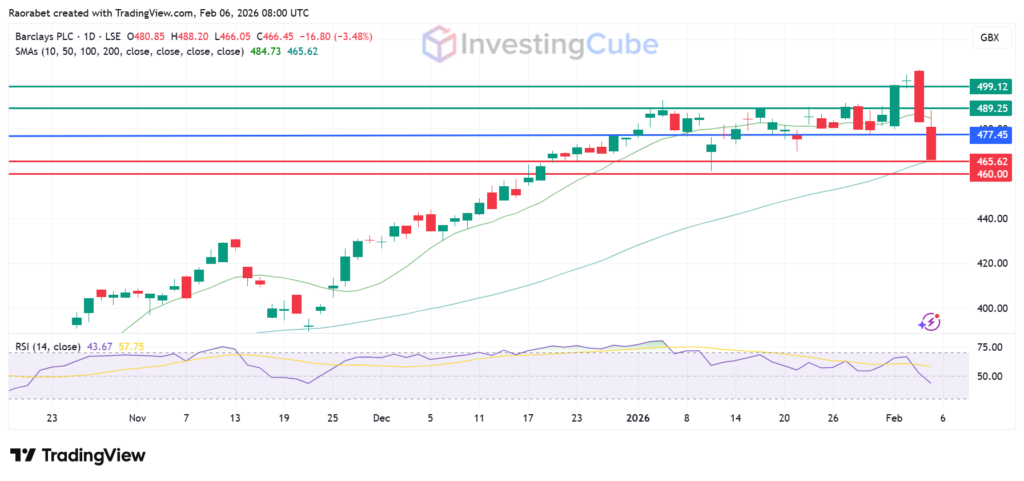

Barclays share price is struggling for upside momentum. It currently pivots at 477.45p and has its primary support at the 50-day SMA at 465.62p. If it goes below that, the stock could fall to the 440p support zone. On the upside, the key immediate resistance it faces is at 489.25p. Traders will want to see it close above this level to signal a move back to near the psychological 500p.

Barclays share price with support and resistance levels on February 6 2026. Created on TradingView

People took profits after a 78% surge in 2025, earnings estimates were lowered because of economic uncertainty, and capital market problems are pressuring revenue.

Not necessarily. Lloyds is a safer income choice, but Barclays has more room to grow through its investment banking part, which tends to do well when global markets expect the economy to recover.

On February 10, management needs to convince the market that they can hit a 12% or even 15% return on equity even though interest rates are falling. This could either help or hurt investor confidence.