- Lloyds Bank was among the most profitable banks in the UK in 2025, with its pre-tax profits rising by 12% to £6.66 billion

- The tide has turned in 2026, and the war in the Middle East has forced the Bank of England (BoE) into making uncomfortable interest rate decisions

- Q2 2026 and beyond will depend on the resolution of the Middle East war and the outcome of Motor Vehicle Sales mishandling claims

Lloyds Bank share price has plummeted, falling more than 6% so far this year and nearly 12% in the past month alone. Yesterday’s small rise of close to 1% brought quiet relief following days of decline. The big question for Q2 2026 is if this will this hold as real stability or simply mark another pause before further drops. We discuss what’s at play and how this could impact the stock in the coming months.

The Iran War and the Rate Reversal No One Expected

The positive momentum at the start of the year has been interrupted by multiple geopolitical events. The most significant is the US-Israeli military action against Iran in late February, which pushed oil and gas prices higher and compelled a reassessment of expectations around Bank of England policy.

Current market forecasts assign about a 50% chance of a BoE rate hike this year, while the Office for Budget Responsibility predicts inflation will reach 3% by year-end, exceeding the Bank of England’s 2% target. This shift from anticipating rate cuts to the possibility of hikes has disrupted the investment case for Lloyds, especially at a sensitive time.

Though the bank benefits from a structural hedge offering some protection, it cannot fully offset the impact. A rate increase triggered by energy price shocks, rather than steady economic growth, differs significantly from the relatively stable higher-rate conditions Lloyds experienced between 2022 and 2024.

Motor Finance Saga Refuses to Resolve

Lloyds Banking Group (LSE: LLOY) currently faces pressure from the Financial Conduct Authority’s investigation into motor finance, with over 12 million agreements eligible for compensation. The bank is still evaluating the situation and will provide updates when appropriate.

The fact that it’s not clear is a problem in and of itself. Lloyds has reserved £1.95 billion for related costs, whereas industry-wide FCA estimates approach £7.5 billion. Adding complexity, about 30,000 customers are preparing to bypass the FCA compensation scheme, opting for a £66 million court claim via Courmacs Legal, citing concerns that the regulator’s approach favors lenders.

Lloyds Bank’s Q2 2026 Outlook

In 2025, Lloyds recorded a 12% increase in pre-tax profits, reaching £6.66 billion, and expects underlying net interest income to rise to around £14.9 billion in 2026 from £13.6 billion in 2025. The bank is planning up to £1.75 billion in share buybacks and raised its 2025 dividend by 15%. These figures indicate financial strength despite prevailing concerns.

Nonetheless, risks remain notably high. Ongoing inflation pressures, geopolitical uncertainties in the Middle East, and a decelerating UK housing market may affect Lloyds’ mortgage and consumer lending segments. Additionally, regulatory scrutiny of capital distribution and potential fiscal policy changes create further unpredictability. Investors may find a cautious, targeted approach more appropriate than broad sector exposure.

Lloyds Bank Share Price Forecast

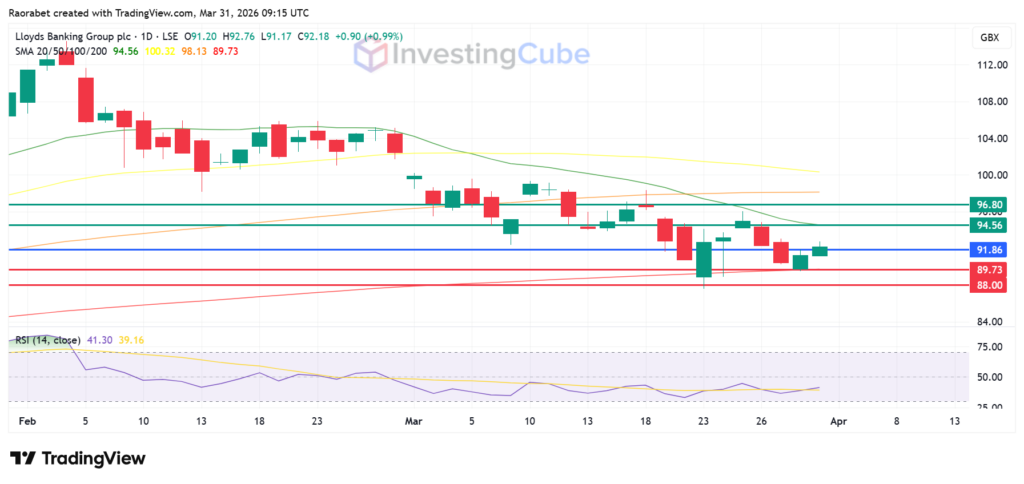

Lloyds Bank RSI is hovering at 40.98, and rising above the signal line, suggesting the stock is in neutral territory. The first hurdle for a rebound is staying above the 91.86p mark (Pivot Point), followed by a heavy resistance zone near the 20-day EMA at 94.0p. Breaking past that will bring 96.80p within reach. Immediate support is found at 89.73p. A breach here could see the price test 88.0p.

Lloyds Bank share price with the key levels of support and resistance on March 31, 2026. Created on TradingView

The FCA’s investigation into motor finance and general economic uncertainty are the main reasons for the drop. High interest rates have raised concerns about a rise in bad debts in Lloyds’ mortgage and loan portfolios, even though they have helped margins.

It is likely a relief rally following the FCA’s finalization of redress rules. While it provides clarity, the stock needs to break above the 92.2p resistance level with volume to confirm a trend reversal.

Persistent inflation forcing the Bank of England to keep rates at 3.75% or higher. This puts immense pressure on UK consumers, potentially leading to higher impairment charges on Lloyds’ vast retail lending book.